Introduction

Life is unpredictable. While we plan for success, growth, and happiness, unexpected events can disrupt even the most carefully structured financial plans. This is where life insurance becomes essential. It is not just a policy—it is a financial safety net that protects your loved ones when you are no longer there to provide for them.

In 2026, life insurance has evolved beyond basic coverage. It now plays a central role in long-term financial planning, wealth protection, and even investment strategies. Whether you are single, married, a parent, or nearing retirement, understanding why life insurance is important can help you make smarter decisions for your future.

This in-depth guide explores every aspect of life insurance, from its core benefits to advanced strategies, helping you understand why it remains one of the most critical financial tools available today.

Understanding Life Insurance

What Is Life Insurance?

Life insurance is a contract between you and an insurance provider. In exchange for regular premium payments, the insurer guarantees a payout (known as a death benefit) to your beneficiaries upon your death.

This payout can be used for various purposes, such as:

- Replacing lost income

- Paying off debts

- Covering funeral expenses

- Funding children’s education

- Maintaining the family’s standard of living

How Life Insurance Works

When you purchase a life insurance policy, you choose:

- Coverage amount (sum assured)

- Policy duration

- Type of insurance

- Beneficiaries

If you pass away during the policy term, your beneficiaries receive the agreed payout. Some policies also offer living benefits, such as cash value accumulation or critical illness coverage.

The Core Importance of Life Insurance

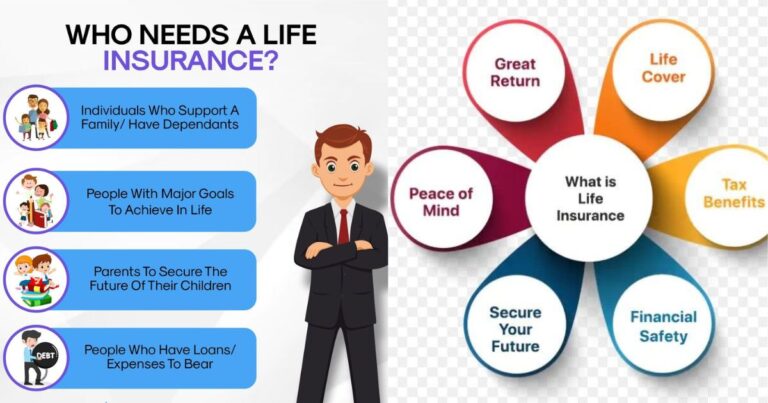

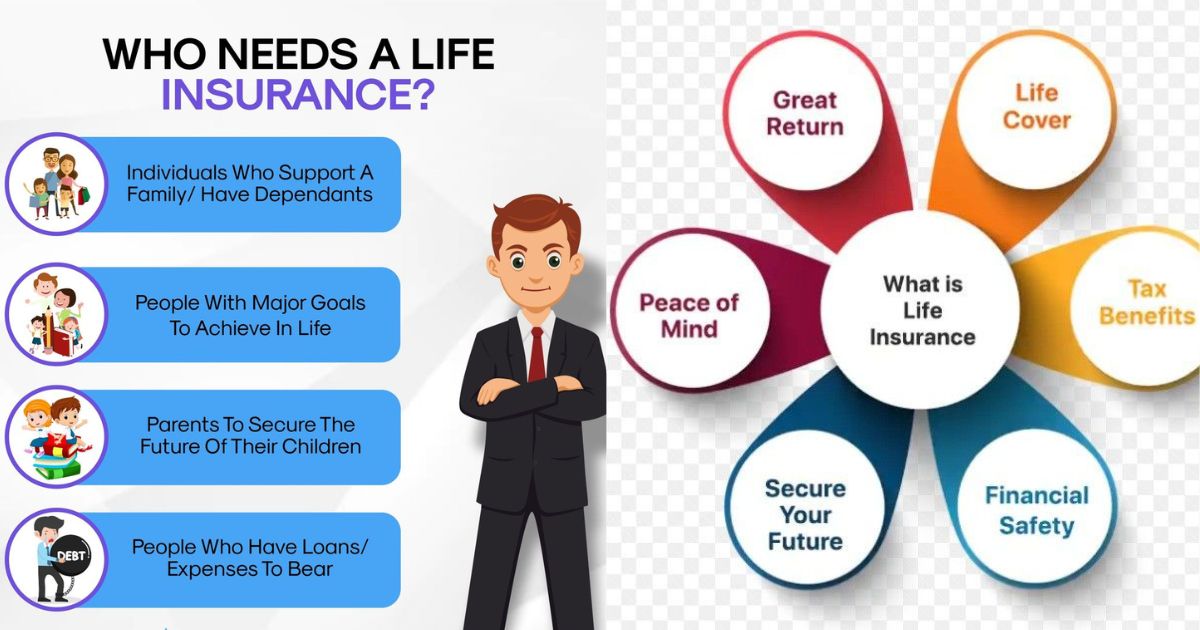

Financial Protection for Your Family

The most important reason to have life insurance is to protect your family financially. If you are the primary income earner, your sudden absence could leave your loved ones struggling to cover daily expenses.

Life insurance ensures that:

- Bills and living costs are covered

- Children can continue their education

- Your spouse maintains financial stability

Income Replacement

Your income supports your household. Without it, your family may face financial hardship. Life insurance replaces your income, providing a steady financial cushion.

Debt Coverage

Many people have debts such as:

- Mortgages

- Car loans

- Credit cards

- Personal loans

Without life insurance, these debts may become a burden for your family. A policy ensures that liabilities are paid off without stress.

Types of Life Insurance

Term Life Insurance

Term life insurance is the simplest and most affordable option.

Key Features

- Coverage for a specific period (e.g., 10–30 years)

- Lower premiums

- No cash value

Who Should Choose It?

- Young professionals

- Families with limited budgets

- Individuals seeking high coverage at low cost

Whole Life Insurance

Whole life insurance provides lifetime coverage and includes a savings component.

Key Features

- Permanent coverage

- Fixed premiums

- Cash value accumulation

Benefits

- Acts as both insurance and investment

- Can be borrowed against

- Offers financial stability

Universal Life Insurance

Universal life insurance offers flexibility in premiums and benefits.

Key Features

- Adjustable premiums

- Flexible death benefits

- Investment component

Ideal For

- Individuals seeking customization

- Long-term financial planners

Life Insurance as a Financial Planning Tool

Wealth Protection

Life insurance protects your accumulated wealth from being depleted due to unexpected events. It ensures that your assets are passed on to your beneficiaries intact.

Estate Planning

Life insurance plays a crucial role in estate planning by:

- Covering estate taxes

- Ensuring fair distribution of assets

- Providing liquidity to heirs

Investment Opportunities

Certain policies build cash value over time. This can be used for:

- Retirement income

- Emergency funds

- Investment diversification

Benefits of Life Insurance in Different Life Stages

Young Adults

Many young people underestimate the importance of life insurance. However, starting early offers several advantages:

- Lower premiums

- Better coverage options

- Long-term financial security

Married Couples

Marriage often brings shared financial responsibilities. Life insurance helps protect your partner from financial stress.

Parents

For parents, life insurance is essential. It ensures that children’s needs are met, even in your absence.

Key Considerations

- Education costs

- Daily living expenses

- Future financial goals

Business Owners

Life insurance can protect businesses by:

- Covering key personnel

- Funding buy-sell agreements

- Ensuring business continuity

Retirees

Even in retirement, life insurance remains relevant. It can:

- Cover final expenses

- Provide inheritance

- Support surviving spouses

Common Myths About Life Insurance

“I Don’t Need Life Insurance”

Many people believe life insurance is unnecessary, especially if they are young or healthy. In reality, these are the best times to secure affordable coverage.

“It’s Too Expensive”

Life insurance is often more affordable than people think, especially term policies.

“My Savings Are Enough”

Savings can be quickly depleted by large expenses. Life insurance provides guaranteed protection.

“Only Breadwinners Need It”

Even non-working individuals contribute significant value (e.g., childcare, household management). Life insurance can cover these contributions.

Key Features to Look for in a Life Insurance Policy

Adequate Coverage

Ensure the policy covers:

- Income replacement

- Debts

- Future expenses

Affordable Premiums

Choose a plan that fits your budget without compromising essential coverage.

Flexibility

Look for policies that allow adjustments as your life changes.

Strong Claim Settlement Ratio

Select insurers known for reliable and fast claim processing.

How to Choose the Right Life Insurance Policy

Step 1: Assess Your Needs

Determine:

- Financial responsibilities

- Number of dependents

- Long-term goals

Step 2: Calculate Coverage Amount

A common rule is to choose coverage that is 10–15 times your annual income.

Step 3: Compare Policies

Evaluate:

- Premiums

- Benefits

- Policy terms

Step 4: Consult an Expert

Financial advisors can help you choose the best plan based on your situation.

Riders and Add-Ons

Life insurance policies often include optional riders that enhance coverage.

Common Riders

- Critical illness rider

- Accidental death benefit

- Disability income rider

- Waiver of premium

These add-ons provide extra protection and flexibility.

Tax Benefits of Life Insurance

Life insurance offers tax advantages in many countries:

- Premiums may be tax-deductible

- Death benefits are often tax-free

- Cash value growth may be tax-deferred

These benefits make life insurance an efficient financial tool.

Risks of Not Having Life Insurance

Without life insurance, your family may face:

- Financial instability

- Debt burdens

- Lifestyle changes

- Limited opportunities for children

The absence of a safety net can have long-term consequences.

Life Insurance and Modern Technology

Digital Policies

You can now purchase and manage policies online بسهولة.

AI-Based Underwriting

Faster approvals and personalized premiums based on data analysis.

Mobile Claims Processing

Quick and easy claims submission through apps.

Tips to Maximize Your Life Insurance Benefits

Start Early

Younger individuals enjoy lower premiums and better options.

Review Regularly

Update your policy after major life events:

- Marriage

- Birth of a child

- Career changes

Avoid Underinsurance

Ensure your coverage is sufficient for your needs.

Maintain Transparency

Provide accurate information to avoid claim issues.

The Future of Life Insurance

Life insurance is becoming more personalized and accessible. Key trends include:

- Usage-based insurance

- Integration with financial apps

- Enhanced customer experience

- Greater transparency

As technology advances, life insurance will continue to evolve, offering better value and convenience.

Conclusion

Life insurance is not just about preparing for the worst—it is about protecting the people you care about most. It provides financial security, peace of mind, and long-term stability for your loved ones.

From income replacement to wealth preservation, life insurance serves multiple purposes that make it indispensable in modern financial planning. Regardless of your age or financial situation, having the right life insurance policy ensures that your family’s future remains secure.

In a world full of uncertainties, life insurance stands as a reliable foundation for financial protection. The sooner you invest in it, the better prepared you will be for whatever life brings.